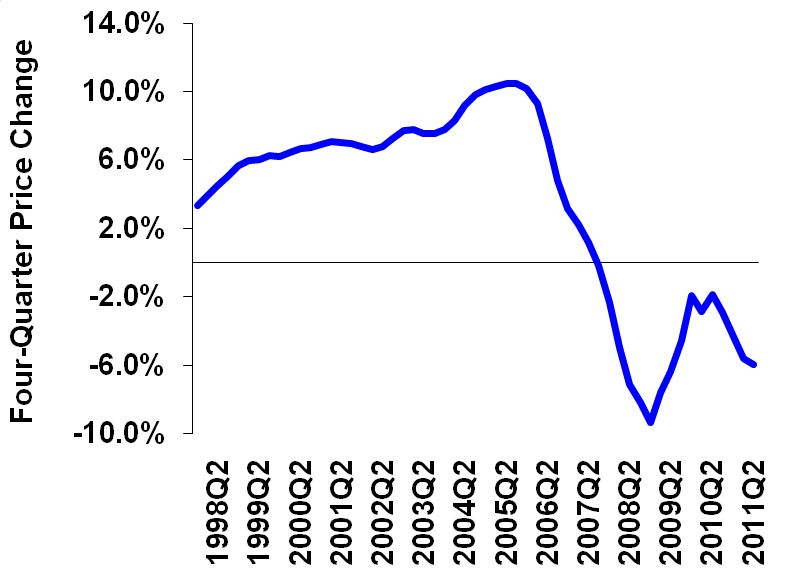

How time flies! It's hard to believe three whole years have passed since the US Treasury stepped in and took over Fannie and Freddie. Three years of insolvency, delinquent mortgages, trial mortgage modifications, robo-signed foreclosure complaints, underwater homeowners and short sales. Three years of Realtors navigating seismic shifts in the real estate landscape with falling home values, board-ups and growing inventories. How time flies indeed.

Happy Anniversary!

So it's been three years - the traditional gift for a third anniversary is leather. Seems like it would be easy to think of a few entities or individuals who deserve getting some good leather, perhaps not of the gift-wrapped variety, but rather in swift delivery across their respective backsides. But in looking for culprits who really is at fault?

How about Wall Street and the derivative guys selling toxic assets repackaged as private-label securities. Or the top-dogs at Fannie and Freddie who orchestrated special insider accommodations and promoted Pollyannaish loan programs in countervention of the tenets of prudent lending. Or public policy-makers in DC who sought to check off items on their social agenda to-do lists by exploiting influence over the GSEs and financial institutions. Then there are the mortgage companies, loan originators, appraisers, sales people, builders, developers, all of us "in the loop" who feverishly pumped transaction volume at record pace through the bulging pipeline during the heady days of the late boom. And oh yeah, lets not forget the borrowers who signed the loan applications and nodded their heads to all those qualification questions about income, source of funds, employment, occupancy and the like.

That's a lot of leather. But the fact is there is no single cause for the collapse we are now tunneling our way through. Top to bottom, everybody donned rose-colored glasses and looked to ride the wave of a seemingly ever-expanding market as far as it would go.

We the People...

Since entering conservatorship in 2008 Fannie and Freddie have received over $153 Billion from the US Treasury. What's that money buying us? Wiggle room, I guess. Allowing time to formulate an orderly dismount from the once-noble experiment in public-/private-sector lending, now become a bucking behemoth, officially in its death throes. Closing short sales and turning over REO inventory we see the micro-deficits as Treasury dollars are doled out dollop by dollop one transaction at a time.

The good news is that each sale is one unit closer to working our way through. It's like the old joke - Q: How do you eat an elephant? A: One bit at a time. My hat is off to everyone in the real estate community as you adapt and reinvent yourselves to serve the American homeowner. It is important to continue the struggle against a flood of challenges and persevere. Because private property is foundational to a free society and real estate is its cornerstone.